Explainers

Parts of the Scottish Budget

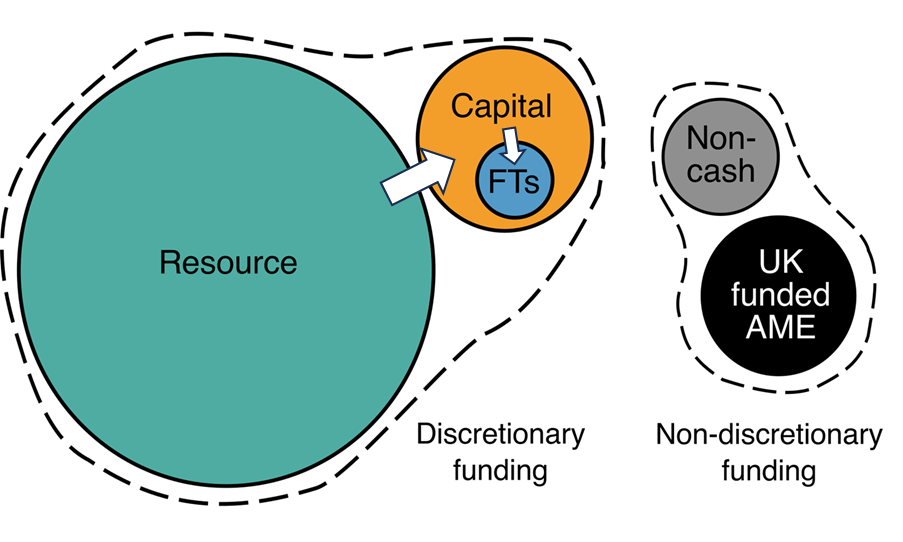

Most of the Scottish Budget is money the Scottish Government decides how to spend. We call this discretionary funding. While its exact share changes each year, on average it is around 90 per cent of the Scottish Budget.

Discretionary funding is divided into three categories based on how each can be spent: resource, capital and financial transactions.

- Resource is to pay for day-to-day running costs, such as grants to local government, transfers to households in the form of devolved social security payments, or staff pay. Most of the Scottish Budget is resource funding.

- Capital can only be spent on long-term investments, such as hospitals, roads and research and development.

- Financial transactions (FTs) are a subset of capital funding which can only be used to create financial assets, such as lending money to or making equity investments in private sector entities.

The rest of funding is set aside for a specific purpose. Because of this, we call it non‑discretionary funding. Even though it is part of the Scottish Budget, we do not include it in our publications because it does not reflect Scottish Government decisions. There are two parts:

- UK-funded Annually Managed Expenditure (AME) is demand-led spending which, while devolved, is fully paid by the UK Government. Two such areas are teachers’ pension payments and student loans.

- Non-cash is a subset of resource funding only available to use for accounting adjustments, such as depreciation of assets.

Watch the Government spending in Scotland video in the explainer’s section to find out more.