In this Insight we highlight two of the more challenging economic issues which will likely influence the Scottish outlook over the next parliament.

These issues are:

- The increase in the number of people not working nor looking for a job (that is, declining labour force participation) due to health reasons, including among young people.

- Ongoing weak productivity growth.

Both of the above could lead to a slowdown in living standards growth.

These developments are of course not unique to Scotland. They have also been affecting the UK and other European economies.

Why does this matter?

A healthy and productive working population, stronger economic growth, and higher incomes help boost tax revenues, making it easier for government to fund public services.

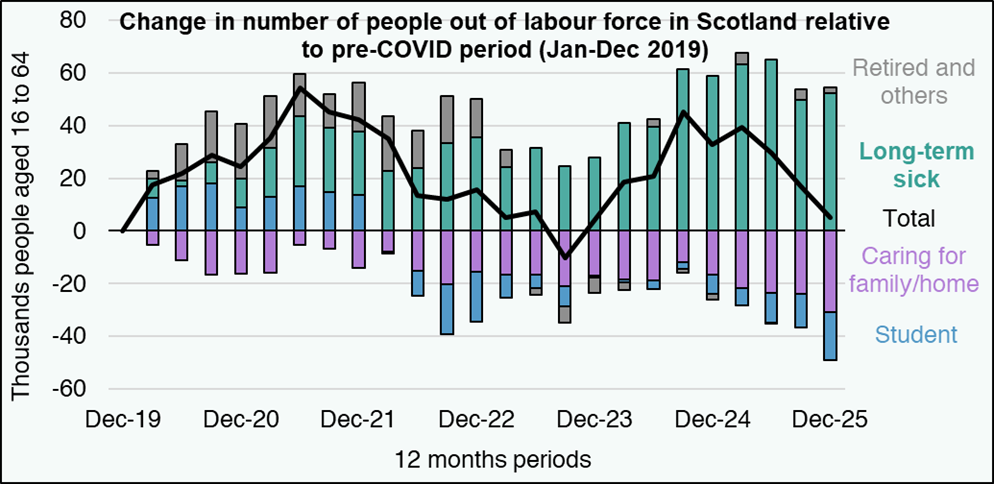

Ill-health on the rise since the COVID-19 pandemic among people not working nor looking for a job

Despite quality issues with the Labour Force Survey, a clear trend in the data has been the rise since the COVID-19 pandemic in ill‑health as a reason for not working nor looking for a job (that is, for being out of the labour force).

As Figure 1 shows, long-term sickness has been increasingly dominant among people who are not working nor looking for a job. This also includes people who were already out of the labour force for another reason but are now reporting long-term sickness as their main reason for not working nor looking for a job.

Alongside this, there has been an increase in disability-related and incapacity‑related benefit claims. However, the link between these trends is uncertain. This is because higher health‑related benefit claims do not necessarily imply lower labour force participation, as many people receiving those benefits are in work while many people who are not in work are not receiving those benefits.

A related trend has been the increase in the number of young people who are not in education, employment or training. This is currently being explored in the Milburn Review commissioned by the UK government.

Addressing these challenges is important in many ways, both for individuals and for the government. In particular, better health can mean more people in work and in good‑quality jobs than might otherwise be the case, as well as reducing demand for public services.

Figure 1: People not working nor looking for a job (out of the labour force) in Scotland by main self-reported reason

Source: Labour Force Survey / Annual Population Survey.

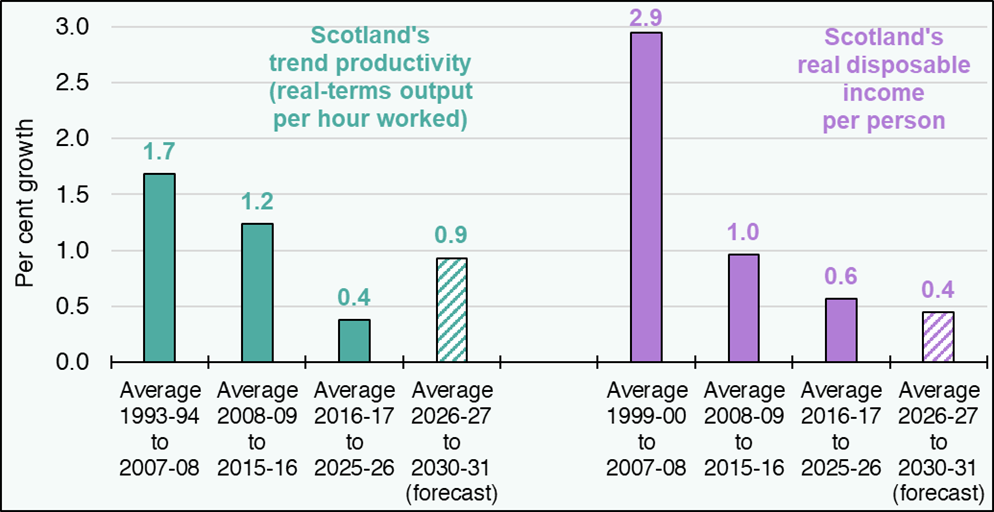

Productivity growing slowly

Productivity measures how much is produced (goods or services) using a set amount of resources, such as workers and equipment. Higher productivity means producing more output with the same resources and is therefore a key ingredient for a growing economy, rising living standards, and increased spending on public services.

Figure 2 shows that productivity growth in Scotland has slowed since the Global Financial Crisis (GFC) of 2008-09, with this trend worsening over the last decade. Since 2016-17, productivity growth has been broadly flat, being further dampened by the shocks from Brexit, the COVID‑19 pandemic, and the energy price crisis of 2022-23.

Looking ahead to the next five years, we expect that productivity growth will remain subdued and will not return to the pre‑GFC average, contributing to a challenging outlook for the Scottish Budget.

Figure 2: Growth in Scotland’s trend productivity and living standards

Source: Scottish Fiscal Commission.

Living standards improving slowly

In line with weak labour force participation and weak productivity growth, living standards – as measured by real disposable income per person – have also grown slowly. Real disposable income per person is a total estimate of how much money, on average, people can spend or save after accounting for tax, borrowing costs such as mortgage interest payments, and inflation.

As Figure 2 also shows, real disposable income per person improved at an average of 3 per cent per year from 1999-00 to 2007-08. Since then, living standards growth has been sluggish, especially over the last decade. It fell sharply in 2022-23 due to rising inflation and interest rates following Russia’s invasion of Ukraine but has since recovered to its 2021-22 level. In our January 2026 forecast, even before current events in the Middle East, we expected this trend of slow growth to continue over the next five years.

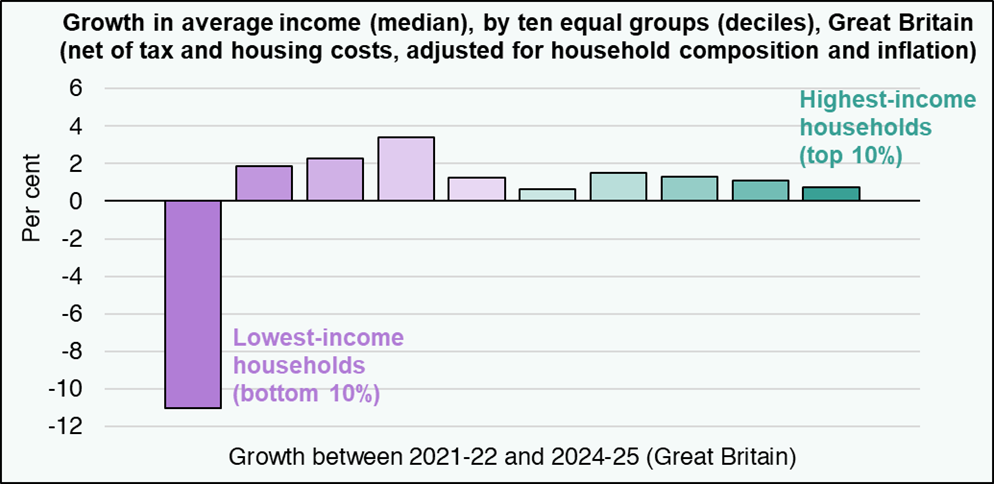

When considering living standards by lower and higher income groups, conditions have varied across different households.

Using an alternative measure of disposable income from the Department for Work and Pensions, broken down by income levels, Figure 3 shows that the lowest‑income households across Great Britain have been hit the hardest by the living standards crisis of 2022-23. This is because they spend a larger share of income on essentials such as energy, food, and housing, for which price levels have increased significantly from 2021‑22.

As well as having equalities implications, this matters for our work as the distribution of earnings growth can affect economic growth, tax revenues, and some social security spending.

The latest energy price shock following events in the Middle East is likely to put further pressure on household finances, particularly for people on lower incomes.

Figure 3: Growth in average disposable income

Source: DWP Families Resources Survey, Households Below Average Income dataset. Accessed on Stat-Xplore.

What’s next?

Focussing on the months ahead, the ongoing crisis in the Middle East means there is significant uncertainty in the economic outlook. While oil prices have fallen somewhat since the highs seen in April 2026, geo-political tensions remain elevated and there are a wide range of possible scenarios that could play out in the Middle East in the coming months. We discussed some of these in our Insight last month. The crisis could amplify the economic challenges discussed in this Insight.

In the longer term, productivity, participation, and resultant living standards are the key determinants of the prospects for Scotland’s economy and public finances. One particular risk is that if the Middle East crisis continues for some time, there could be knock-on effects to productivity, participation and, in turn, living standards for years to come.

We will continue to analyse and discuss these issues in our future work, including how they might be impacted by other shocks and factors such as Artificial Intelligence, an ageing population, and other economic and societal changes. We look forward to supporting the new Parliament in understanding these dynamics and what they mean for Scotland’s economic and fiscal outlook.