Recent events in the Middle East have resulted in heightened geopolitical uncertainty and concerns over an energy price shock. Similar to what happened in 2022 following the Russian invasion of Ukraine, we have seen rapidly increasing energy prices, which could significantly affect the global economy.

In April the price of Brent crude oil (the most widely referenced global oil trading benchmark) rose above $115 per barrel, around double the price seen at the end of 2025. Petrol and diesel prices have increased sharply since the start of 2026. Global food production is also vulnerable, because crude oil is used to make fertilisers and other products critical to modern food production. Higher fuel and energy costs are affecting both businesses and households, and prices are likely to start rising across the economy – though we have not seen a significant effect in the inflation data yet, which is currently available up to April. So far, we believe most of the impact in the UK has been on prices, and there have not yet been any significant physical shortages of food and other goods.

The broader economic impact will depend in part on how households, businesses, and the Bank of England respond to rising energy and input costs. If the shock is thought to be temporary, there may be only small changes to behaviours. If it is seen as lasting longer, we may see stronger responses – for example, higher wage demands from employees, businesses charging more to recover higher costs, or higher interest rates to try to control inflation.

The depth and duration of the economic shock will depend on how the conflict in the Middle East evolves over the coming months. A relatively short-lived crisis may result only in an economic slowdown. However, even with a quick resolution to the conflict, the effects are likely to be felt for several months, as it will take time for the global supply of oil to normalise. We could continue to see issues with oil supply and knock-on effects to those sectors dependent on fossil fuels. A longer conflict could push some economies into recession.

Even before the escalation in the Middle East, there were concerns about the economic outlook. Globally, there continued to be uncertainty around tariffs. In the UK, inflation was already above its 2 per cent target. In Scotland, consumer confidence was negative, while both pay growth and employment were slowing.

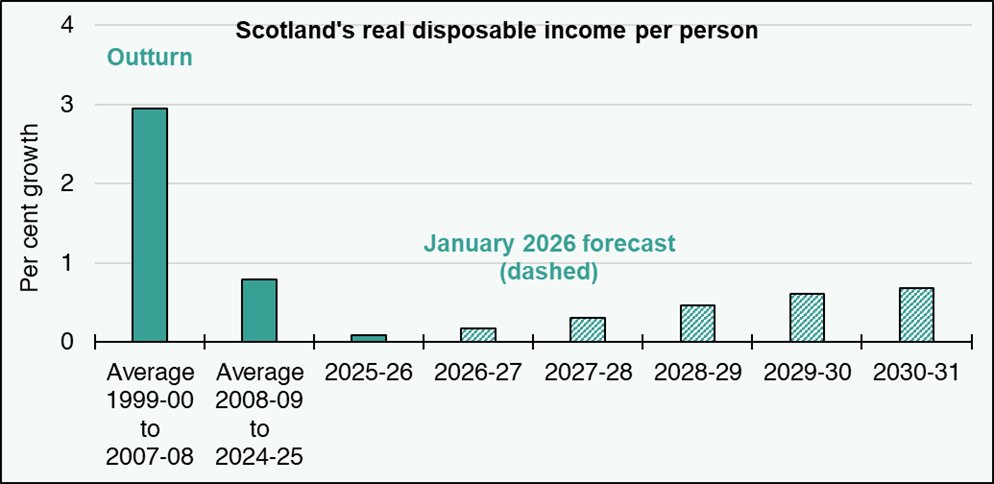

As Figure 1 shows, our January 2026 forecast projected continued weak growth in real disposable income per person – a key measure of living standards. The Middle East conflict and a prolonged energy price shock causing higher inflation could mean even weaker growth in real disposable incomes in the future.

Figure 1: Growth in real disposable income per person (per cent)

Source: Scottish Fiscal Commission.

Scottish fiscal outlook

Rising prices will put pressure on all government budgets in several ways, and Scotland will share these.

Across the UK, social security payments and pensions linked to inflation will increase. The cost of delivering public services will also rise, meaning higher spending will be required to maintain existing provision. There may also be increased demand for higher public sector pay. Depending on the extent of the impact on household finances, the UK Government may introduce additional support measures.

While spending pressures will increase, inflation can also boost tax revenues. This is particularly relevant for Income Tax, where thresholds remain frozen across the UK. If inflation leads to increases in earnings, this can lead to stronger Income Tax receipts through fiscal drag.

For Scotland, how all this comes together depends on the fiscal framework. The Scottish Government’s funding from the UK Government will depend on how the UK Government responds to these challenges. If the UK spends more in England on areas devolved to Scotland such as health and education, then the Scottish budget will increase. But if the UK Government increases taxes already devolved to Scotland, UK funding to Scotland will fall and the effect on the Scottish Budget will depend on whether the Scottish Government follows a similar tax policy and how much that raises.

Concluding thoughts

As has been seen in the highly volatile oil price movements of recent months, events in the Middle East have introduced considerable additional economic uncertainty. At the time of publication on 21 May 2026, the Brent Crude oil price has fallen back from recent highs, but remains elevated. This highlights the considerable challenges involved in forecasting during periods of global volatility. Given the lag in official economic statistics, the full impact of the conflict is not yet visible in the data. Consumer price inflation in April fell to 2.8 per cent, compared to 3.3 per cent in March and 3.0 per cent in February, because of the anticipated reduction in the Ofgem energy price cap for April to June. However, underneath this overall rate, there was a large increase in motor fuel price inflation, reflecting the recent rises in petrol and diesel prices. The Ofgem cap is also expected to go up when it is next updated in July.

We will revisit the economic and fiscal impact of the Middle East conflict in our next Fiscal Update, scheduled for 25 August 2026, and will incorporate the effects into future forecasts, including those accompanying the next Scottish Budget.