Last week, Parliament agreed the Scottish Rate Resolution, which sets Scottish income tax rates and bands for 2026-27. Revenues from Scottish income tax fund the Scottish Budget and the tax rates being set means the 2026-27 Budget Bill can now proceed to its final parliamentary ‘stage 3’ on Wednesday this week.

This Insight considers how the Scottish Government has used devolved non-savings, non-dividend income tax powers to generate additional revenues and funding for the Scottish Budget.

More complex but more progressive

Since Scottish income tax was devolved, the Scottish Government has made changes to increase tax rates and create a more ‘progressive’ income tax system in Scotland. Progressive simply means higher earners pay a larger percentage of their income in tax than lower earners. However, it has also made the income tax system more complicated than in the rest of the UK.

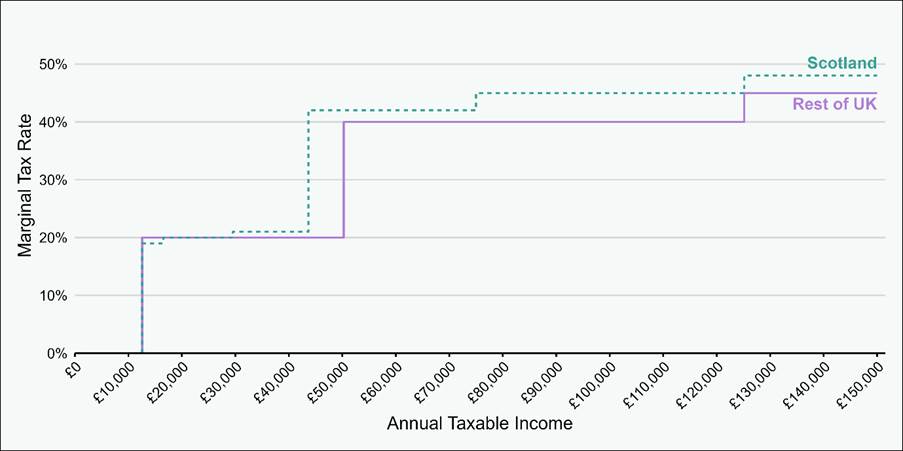

Scotland has 6 tax bands in 2026-27 compared with 3 in the rest of UK

Figure 1: Scottish and rest of UK Income tax rates and bands

Figure 1 shows that Scotland has higher rates of tax on higher income levels than the rest of the UK. For example, Scotland has an advanced rate tax of 45% which starts on incomes of £75,001 and a top rate tax of 48% which starts on incomes over £125,140. This compares with no advanced rate in the rest of the UK and an additional rate of 45% on incomes over £125,140.

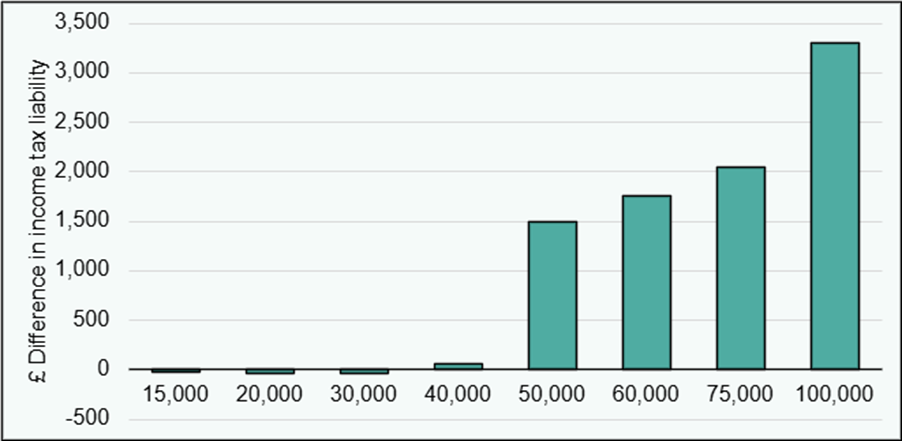

Scottish taxpayers therefore pay different amounts of income tax compared with those living in the rest of the UK. This is shown in figure 2.

Figure 2: £ difference in income tax paid in Scotland compared with rest of UK

While the changes to the income tax system benefited the Scottish Budget by around £1 billion in extra funding in 2026-27, they have also created an important longer term revenue raising potential. This has come from a concept known as ‘fiscal drag’.

What is fiscal drag?

Fiscal drag occurs when the government chooses to freeze or adjust income tax thresholds by less than average wage growth. This means that as people’s income increases over time, more and more people are ‘dragged’ into paying tax at higher rates. This leads to taxpayers paying an increasing share of their income as tax and tax revenues rising faster than earnings growth.

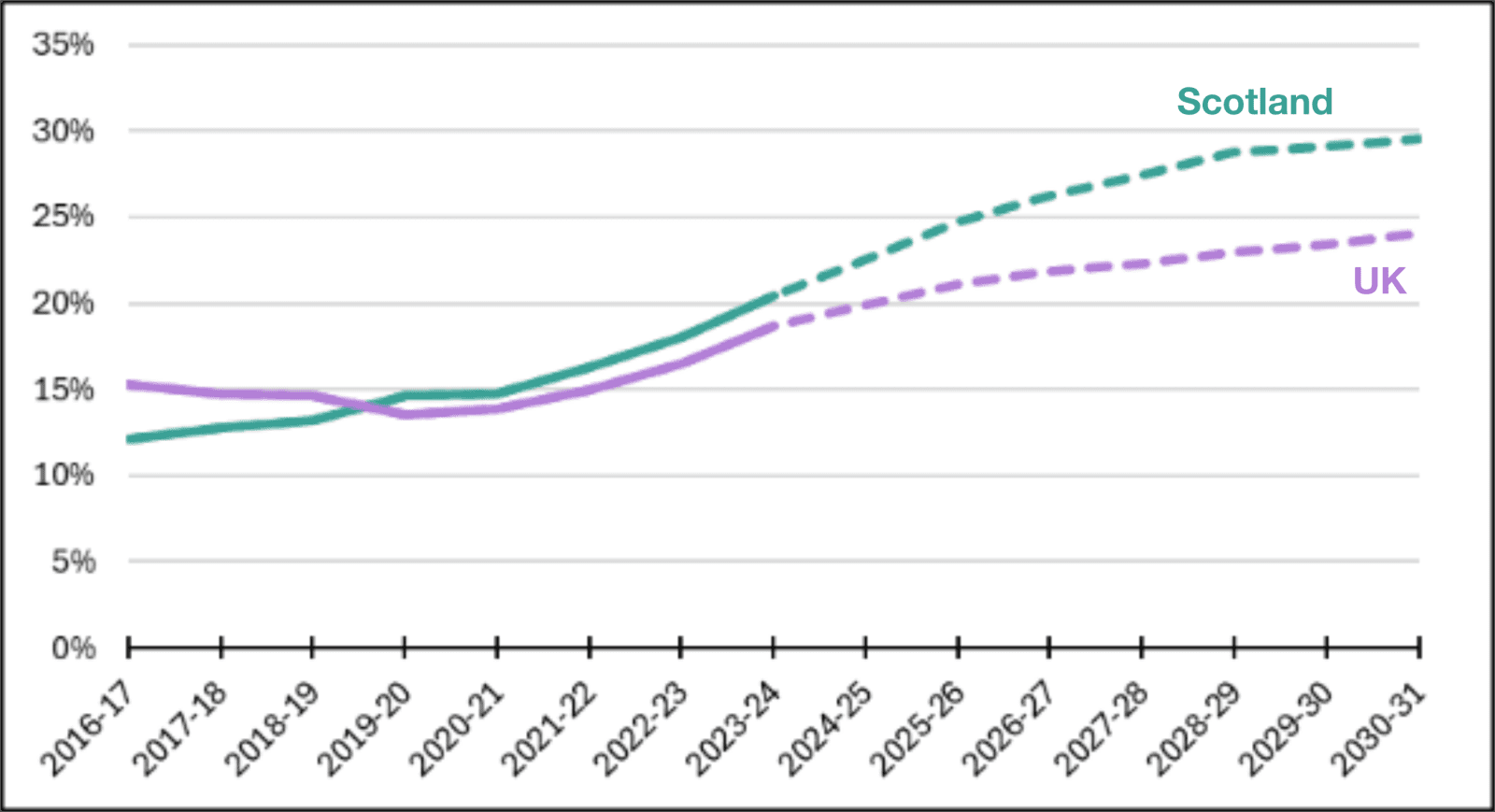

Fiscal drag is not unique to Scotland – it has happened across the UK – but Scotland’s more progressive system means a comparatively larger number of taxpayers being dragged into higher tax bands. The share of Scottish income tax-payers that fall into higher rate or above tax bands has overtaken the UK as a whole. This is shown in figure 3 below.

Figure 3: Share of all income taxpayers paying higher rate tax or above

When income tax powers were first devolved to the Scottish Parliament in 2016-17, 12.1 per cent of Scottish income taxpayers were higher rate taxpayers compared with 15.3 per cent in the UK as a whole. This position had flipped by 2019-20 with more higher rate taxpayers in Scotland. In 2026-27 more than one in four Scottish income taxpayers are expected to be higher rate taxpayers (26.3 per cent) compared with just over one in five in the UK as whole (21.9 per cent).

One real world implication of this is that an increasing share of Scottish taxpayers are paying higher rates of tax – currently projected to be around 1 million Scots by the end of the decade. It also means taxpayers who in the past were not traditionally higher rate taxpayers (like some nurses and teacher grades) are now paying higher rates.

Tax debates likely to continue

The general approach of the current Scottish Government’s tax policy since powers were devolved has been to make changes at the lower end of the tax distribution to make tax liabilities in Scotland a bit smaller than in the rest of the UK. At the same time, the Scottish Government has increased tax rates as taxpayers move up the distribution.

This Insight has discussed policy in relation to income tax. However, the use of fiscal drag has also been applied to Land and Buildings Transaction tax (LBTT) policy (formerly known as Stamp Duty). For example, properties up to £145,000 are exempt from LBTT in Scotland, while LBTT is paid at 12 per cent on the property value over £750,000. These thresholds are unchanged since 2015. Like income tax, this means that as house prices rise, more and more housebuyers are paying LBTT, and paying LBTT at higher rates.

Debates on tax policies are likely to be prominent in the upcoming election campaign and will be a key element of any new administration’s revenue raising considerations.